Is China on its way to a beautiful de-leveraging?

Macro Insight

QuantCube’s latest insights into China’s economic outlook

Lifting Covid-19 restrictions was meant to be the biggest economic event this year in China. Instead, China’s post-pandemic recovery has fallen away quickly, raising questions about the sustainability of its growth model based on investment and debt. Indeed, during the first three quarters of 2023, Chinese economic activity was challenged by increasingly significant factors both domestically and globally. On the domestic front, a full-blown debt crisis in the real estate sector and consequently a significant drop in household and investor confidence hindered its economic rebound. This was further exacerbated by increasingly weak global demand. As a result, policymakers in China were forced to respond with a range of new economic stimuli to revive domestic demand, particularly by easing monetary and housing policy and accelerating the government’s spending on investment. Although significant measures were introduced by the government to boost the economy, there is a growing concern about China’s ability to achieve its 5% economic growth target for this year.

Private consumption - failing to gain traction

China’s post-Covid recovery was largely driven by rising domestic demand. However, it seems that this consumption-led growth did not last for long. Exhibit 1 shows the evolution of the QuantCube Sectoral Consumption Nowcast in China. Its components track private consumption in real-time at both country and sectoral levels by leveraging alternative data such as web search queries, people’s movements (based on transportation data) and consumer reviews. The results are updated daily to provide insights into current consumption trends, ahead of the publication of official numbers.

As expected, internal demand for transport, and cultural and recreation activities skyrocketed right after Covid restrictive measures were lifted; however, the encouraging trend on Chinese consumption growth observed in Q1 2023 was short-lived and it petered out quickly in the spring. The worsening outlook in the real-estate sector seems to have negatively impacted households’ confidence. Indeed, the current state of the housing sector hints at a balance sheet recession as experienced in Germany and Japan during the 1990s, and more recently in the US during 2008 when households adopted a long-term focus on reducing debt, leading to a prolonged decline in housing investment. The term "balance sheet recession" was popularised by economist Richard Koo to describe a scenario where high levels of private sector debt leads businesses and households to focus on saving and debt repayment rather than on spending or investing. During this period, even with zero or near-zero interest rates, the private sector does not increase borrowing. Instead, they prioritise debt repayment and saving. If households and businesses are focused on saving and paying down debt, they're not spending on goods and services. This lack of spending can lead to a decline in production, job losses, and a vicious cycle of further reduced spending, notably on the consumption of durable goods highly related to housing (appliances, furniture, etc.) and can often explain a reduction in new households forming, due to adverse economic conditions and poor confidence. The Chinese economy currently seems to be showing the symptoms of a balance sheet recession with a quickly deteriorating outlook for consumption. Despite the government’s latest financial stimulus, during October our data indicates a persistent deceleration across all sectors, notably in transportation. Exhibit 2 shows the evolution of QuantCube's Air Traffic Nowcast, one of the components of the QuantCube Consumption Nowcast for the transportation sector. It monitors real-time flight data, encompassing flights to and from China, along with domestic Chinese flights. The indicator is recording air traffic activity well below pre-pandemic levels (-35% YoY as of October 30). It is worrying that the recent Golden Week holiday period (October 1 – 7) failed to boost the demand for air travel and that air traffic activity continues to be subdued.

Labour market - job openings are stuck in negative territory in all sectors

It appears that weak consumer confidence is also exacerbated by a struggling job market, plagued by very high youth unemployment. The Chinese government suspended the publication of data for youth unemployment in August last year, so we used job posting data to examine current labour market conditions. At QuantCube, we collect and analyse thousands of job postings every day to track new job offers in real-time at both national and sectoral level. Exhibit 3 shows the evolution of the QuantCube Job Openings Nowcast for key sectors. It seems that the labour market in China remains weak, with job openings in all sectors showing negative growth compared to last year. So far this year we observe no sign of recovery, suggesting that the youth unemployment crisis may not be solved anytime soon.

Ongoing housing crisis is a serious drag

China's debt-laden property sector represents 40% of national GDP. The sector remains one of the most significant obstacles for China’s economic recovery. As we examined in Exhibit 1 and 3 previously, housing demand has experienced a sharp and sustained decline, while job openings in the real estate sector have recorded a staggering -45% decline compared to the previous year. In our view, the government’s efforts to stabilise the sector have yielded limited results so far. The sector's troubles, which started nearly three years ago, were caused by two issues: a challenge in securing developer funding and the weakened demand for housing in general. The ongoing liquidity crunch among developers, including the default of a leading developer in China, Country Garden Holdings Co., seems to have eroded the confidence of homebuyers. As households become increasingly pessimistic about the property sector, they are shifting their savings from housing investments to bank deposits.

The enduring slump in housing demand and the resulting deceleration in construction projects are also evident when looking at trends in China's iron ore import activities. Exhibit 4 shows the QuantCube Iron Ore Imports Nowcast for China. The indicator harnesses real-time AIS (Automatic Identification Systems) maritime data from the ports used by top exporters and importers, and tracks the movements of bulk carriers involved in the transportation of iron ore. The indicator is updated on a daily basis and provides early insights into the current state of commodity imports and exports in a given country. Over the past two months, the indicator has recorded a significant decrease in iron ore imports, and it is currently showing a -5% decline compared to the same period last year (as of October 30). Iron ore is the key raw material needed to produce steel, which is widely used in construction projects. The real estate and construction sectors account for over one third of China’s demand for iron ore. The decline in iron ore imports suggests that construction activity in China continues to be weak.

China’s industrial activity – still expanding supported by resilient exports

While indicators for domestic consumption and construction in China have a negative outlook in line with a balance sheet recession, other nowcasting indicators from QuantCube are showing a slight improvement in factory and trade activities. This suggests that the Chinese manufacturing sector has potentially bottomed out, supported by external trade.

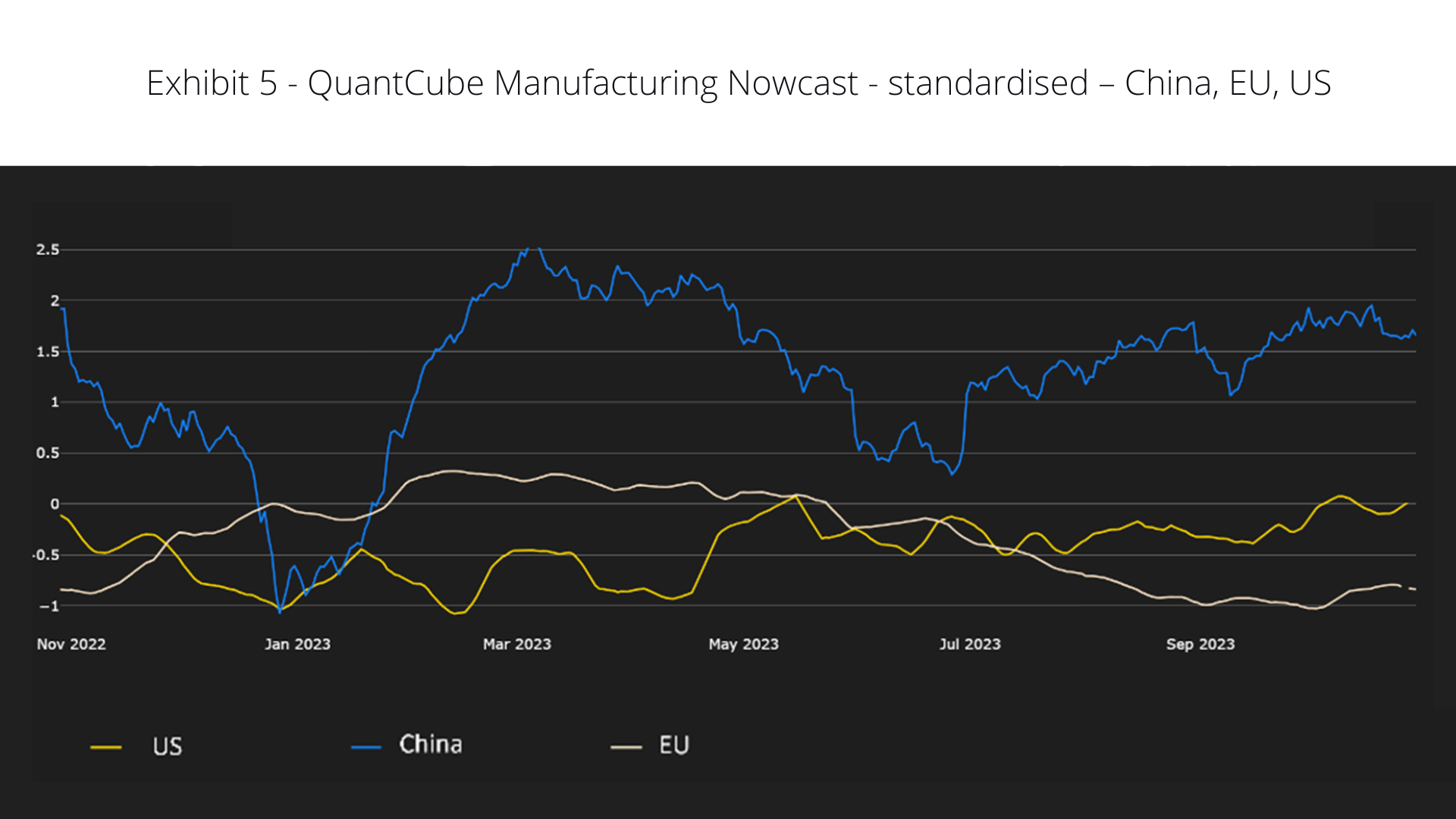

The QuantCube Manufacturing Nowcast (QMN) indicator analyses real-time textual data including newspaper stories, financial news, and specialised publications, using our proprietary multilingual Natural Language Processing (NLP) algorithms. It leverages our advanced alternative data processing technology, which is designed to isolate and analyse key subjects for the industrial sector such as new orders, production and employment data, export backlogs and inventories. Updated daily, the standardized QMN indicator measures sentiment on the current state of the manufacturing sector at the country level: when the QMN is greater than 0, it indicates an expansion in the manufacturing activity.

As Exhibit 5 shows, QMN China currently indicates that manufacturing activity in China is still expanding, notably surpassing the depressed trends in the US and EU, where industrial activity continues to contract.

Based on the satellite data analytics for industrial cities and ports, we can see similar trends.

For instance, over the largest industrial port in the northern part of China, Qingdao, we observe a higher density of NO2 on November 1, 2023, compared to October 23, 2022 as Exhibit 6 indicates. NO2 is a polluting gas emitted by the heavy industry sector, therefore, this suggests increased industrial activity in this region of China.

AIS data insights: demand for Chinese goods strongly supported by emerging countries

The analysis of several real-time indicators in the previous section has underscored the lukewarm state of domestic demand in China. Simultaneously, the demand for Chinese exports of goods has been resilient despite the weakened demand from key trade partners (US and Europe) as a result of a persistent cost of living crisis and monetary tightening.

So which countries are consuming Chinese goods and supporting Chinese manufacturers?

To gain insights into the shift in export partners for Chinese goods, we used AIS data to monitor the number of container arrivals from China across various countries as per Exhibit 7. Interestingly, Chinese exports to emerging economies such as India and Indonesia seem to have been counterbalancing weakened demand in Europe. This has helped to maintain total container exports at a relatively stable level. As the demand in the US recovers, it seems that China’s overall export levels started to recently trend upwards.

In summary, China's debt-laden property sector continues to be the most significant threat to its economic recovery. While there is a certain sign of stability such as the resilience in factory activity, overall recovery remains fragile so far. This was further exacerbated by the financial challenges faced by property developers, which in turn contributed to the weakness in private spending and consumption. In our view it is imperative for China to accelerate the longer-term fiscal reforms with an aim to move the Chinese economy away from an excess investment-driven economy with a more stable consumer-driven growth model.

For the time being, China still seems to heavily rely on foreign consumers to bolster its economic health. Will China remain as the world growth leader? We will wait and see.